The goal of personal auto insurance pricing and underwriting is to define precise risk categories and use those categories to accurately calculate a policyholder’s premium. While pricing actuaries and underwriters take many rating factors into account, one important factor is often missing: a policyholder’s mileage. This blog post explores which role mileage plays as a rating factor today, why it should be given much higher importance, and how insurers can reliably take their policyholders’ mileage into account when calculating insurance rates.

Personal auto insurance rating factors

Pricing actuaries take into account various vehicle and driving factors when determining different auto insurance risk categories. These vehicle and driving factors include a car’s make, model, and age as well as the policyholder’s driving record. Depending on the state, insurers also take into account so-called non-driving factors, such as vehicle owner’s age, credit score, location, gender, marital status, level of education, occupation, and whether they are a renter or a homeowner.

Non-driving rating factors can have a large impact on a policyholder’s rate. For example, by improving their credit score by one tier, policyholders can reduce their insurance premium by as much as 17%.

Mileage as a rating factor

In most U.S. states except California, annual mileage has very little effect on the price of a policyholder’s premium. The state of California requires by law that insurers use mileage as their second auto insurance rating factor. In most other U.S. states, however, mileage doesn’t get as highly rated as a policyholder’s age, driving history, credit score, driving experience, location, gender, and insurance history. On a national average, policyholders who drive more than 15,000 miles per year pay only $92 more than policyholders who drive fewer than 7,500 miles per year—a small difference considering that their annual mileage is at least twice as high.

The reason why mileage doesn’t get rated higher except when required by state law is that it is difficult to verify. When asked to self-report their annual mileage, more than half of policyholders state an incorrect number, and a quarter of them understate their annual mileage by 6,000 miles or more. Mileage verification methods, such as uploading a photo of the car’s odometer reading or installing an aftermarket hardware device in the vehicle, are bothersome for policyholders and expensive for insurance providers to introduce and scale.

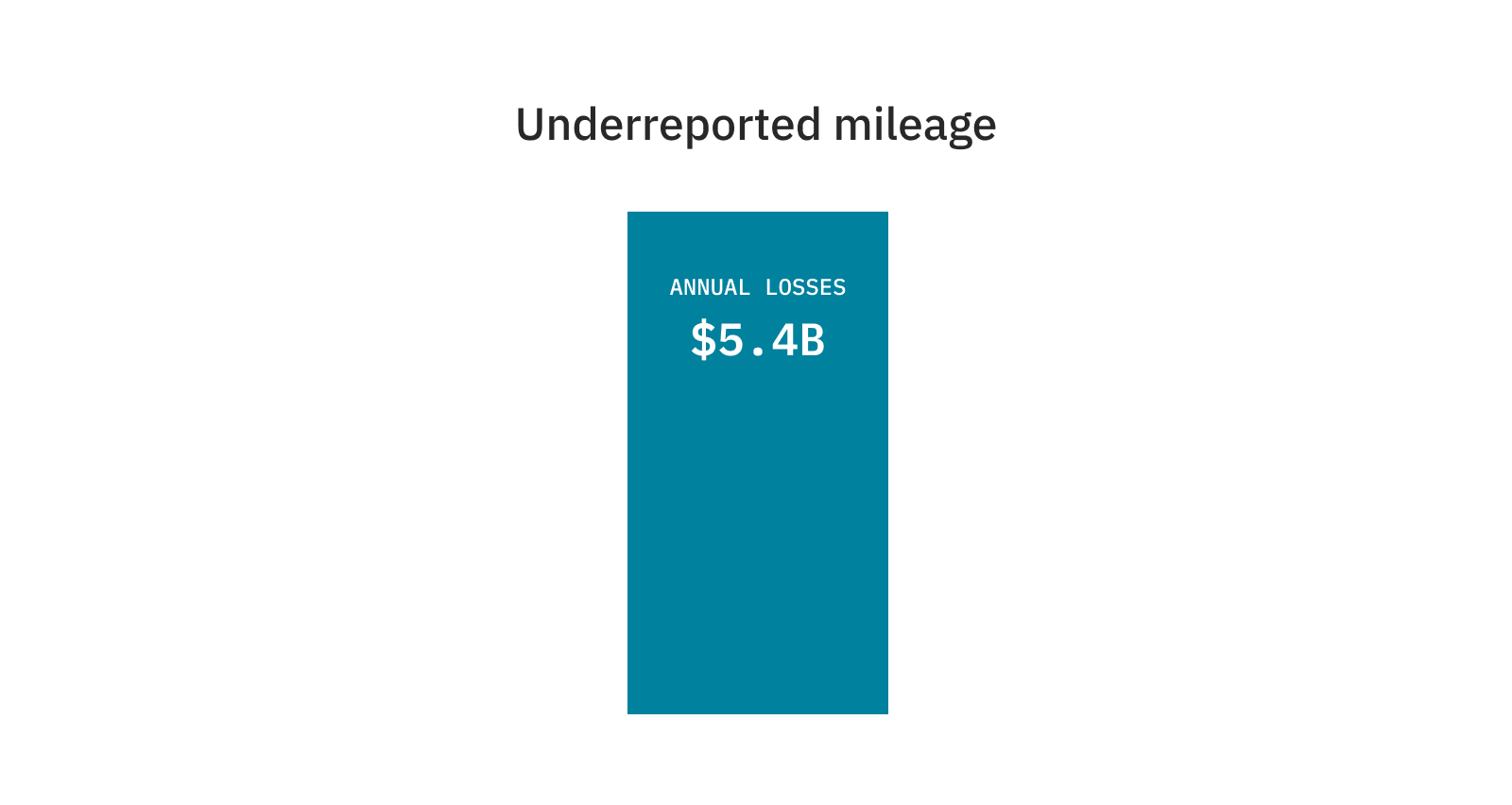

Although mileage is difficult to verify and thus rarely among the most influential rating factors, insurers should start recognizing its importance. There is a clear correlation between the number of miles a policyholder drives and the number of claims they file. When avoiding to take mileage into account just because it is hard to verify, insurers create more problems than they solve. In fact, insurance providers in the U.S. lose $5.4 billion every year just due to underreported mileage.

How to easily and accurately verify mileage

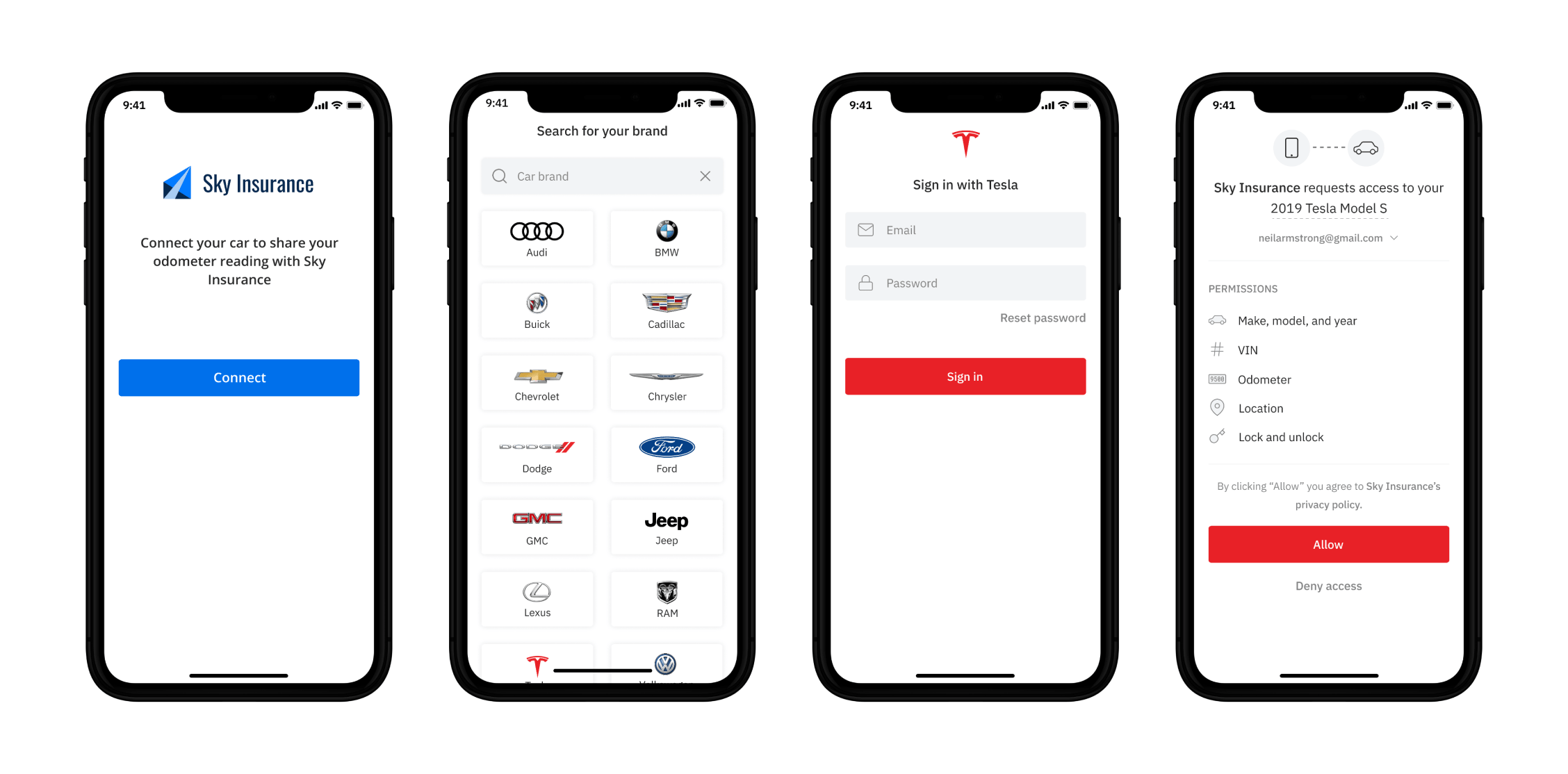

In order to utilize mileage as a more important rating factor, insurers need a way to easily and accurate verify how much their policyholders drive their vehicles. APIs like the Smartcar API help insurers do exactly that. Our technology has allowed insurers like CoverMe and Paydrive to instantly and accurately verify their policyholders’ mileage while staying cost-efficient and ensuring a simple user experience for policyholders.

Policyholders can connect their vehicle and agree to share their odometer reading with just three clicks from the insurer’s web portal or mobile app. The insurer can then automatically retrieve the exact odometer reading from the vehicle’s instrument cluster on a monthly or annual basis.

Smartcar’s all-digital experience makes mileage verification easy, instant, cost-efficient, and 100% accurate—without the need for any additional technology like aftermarket hardware. With a convenient and accurate way to verify their policyholders’ mileage, insurers are finally able to take mileage into account as a reliably rating factor, making their policy pricing and underwriting as accurate as never before.