Vehicle identification numbers (VINs) play an essential but often overlooked role in auto insurance policies. While policyholders are required to provide their vehicle’s VIN when purchasing a new policy, many insurers don’t verify the provided information. As a result, more than 5% of auto insurance policies have an invalid VIN on file.

In this blog post, we’ll explore which role VINs play in auto insurance policies, what happens if a policyholder’s VIN is invalid, and how insurers can easily verify a vehicle’s VIN to address a $2 billion annual problem.

The role of VINs in auto insurance policies

There are a number of reasons why knowing and verifying a policyholder’s VIN is important for insurance providers:

- Pricing policies: Knowing a vehicle’s VIN allows insurers to check whether the make, model, and other information that a policyholder provided are correct, and to adjust their monthly premium accordingly.

- Detecting staged vehicle titles: In addition to achieving more accurate pricing, verifying a policyholder’s VIN can uncover issues in the vehicle’s history, for example, if it has been reported stolen or has a branded title.

- Following regulatory compliance: Some U.S. states require insurers to report all their policy numbers and VINs in an effort to detect uninsured vehicles.

The impact of invalid VINs

When asking a policyholder for their vehicle’s VIN, some insurers don’t verify the reported information. As long alphanumeric strings are prone to manual typing errors, around 5% of all auto insurance policies end up having invalid VINs associated with them. While this seems like a small percentage, the impact that invalid VINs can cause for insurers and their customers is quite severe.

An insurer who doesn’t verify their policyholders’ VINs is unable to double-check important information, resulting in inaccurate rates. The insurer might also report an incorrect VIN to the state, which can cause the policyholder problems regarding proof of insurance. Further problems can occur when the policyholder files a claim and the invalid VIN gets uncovered during that process.

All in all, incorrect VIN reporting leaves auto insurers with unnecessary work and unhappy customers. In fact, the American auto insurance industry loses around $2.1 billion dollars per year just due to incorrect VIN reporting.

How to verify a policyholder’s VIN

There are many ways to verify a policyholder’s VIN and prevent incorrect reporting. Different options range from hardware devices like OBD-II dongles, which policyholders need to install in their vehicles and which allow insurers to read a range of other information apart from the vehicle’s VIN, to VIN decoders, which reveal whether or not the policyholder has provided a valid VIN as well as which make, model, and trim is associated with the provided VIN.

Smartcar provides a solution that doesn’t require hardware like many other telematics solutions, and that still allows insurers to retrieve the VIN directly from each policyholder’s vehicle. Here’s what you need to know about verifying VINs with the Smartcar API:

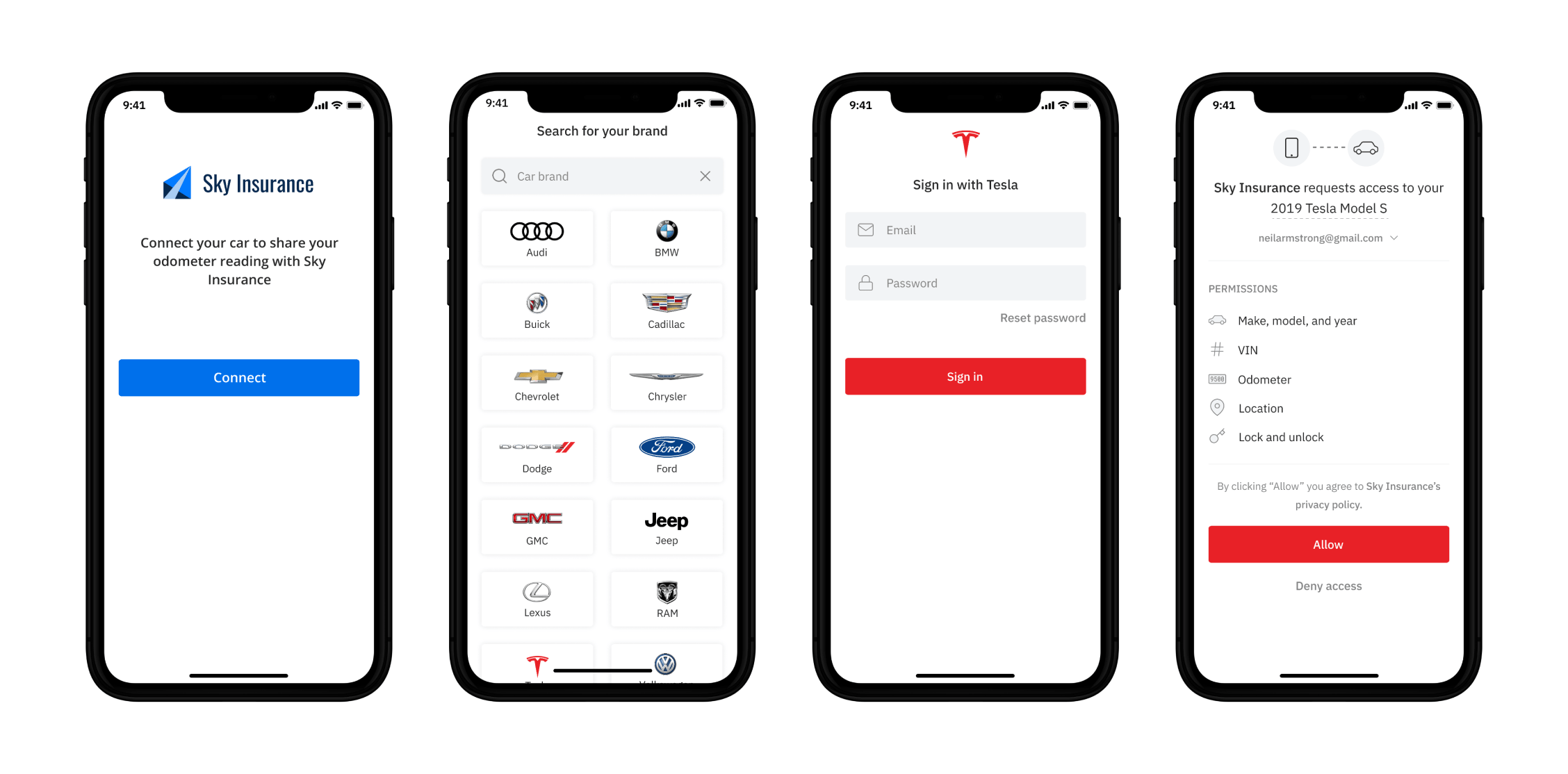

When a policyholder purchases a new policy, the insurer can propose them to link their car to the insurance app using Smartcar. The policyholder links their car with three clicks and reviews exactly which information the insurance application requests access to. Once the policyholder gives their consent, the insurer can retrieve important information such as the vehicle’s VIN, mileage, location, and fuel tank level directly from the vehicle.

The insurance provider now detects incorrectly provided VINs by verifying each policyholder’s vehicle information. If an incorrect VIN is discovered, the insurer can easily replace erroneous information with the vehicle’s actual data. They can then notify their underwriting department to adjust the policy rate, use VIN decoders to check the vehicle’s title history, and update their report to state regulators if necessary.

All in all, invalid VINs are a severe problem that insurance providers often forget about. Using Smartcar’s VIN API, insurers can address a $2 billion annual problem with a single hardware-free solution while improving internal efficiency, compliance, and customer satisfaction.